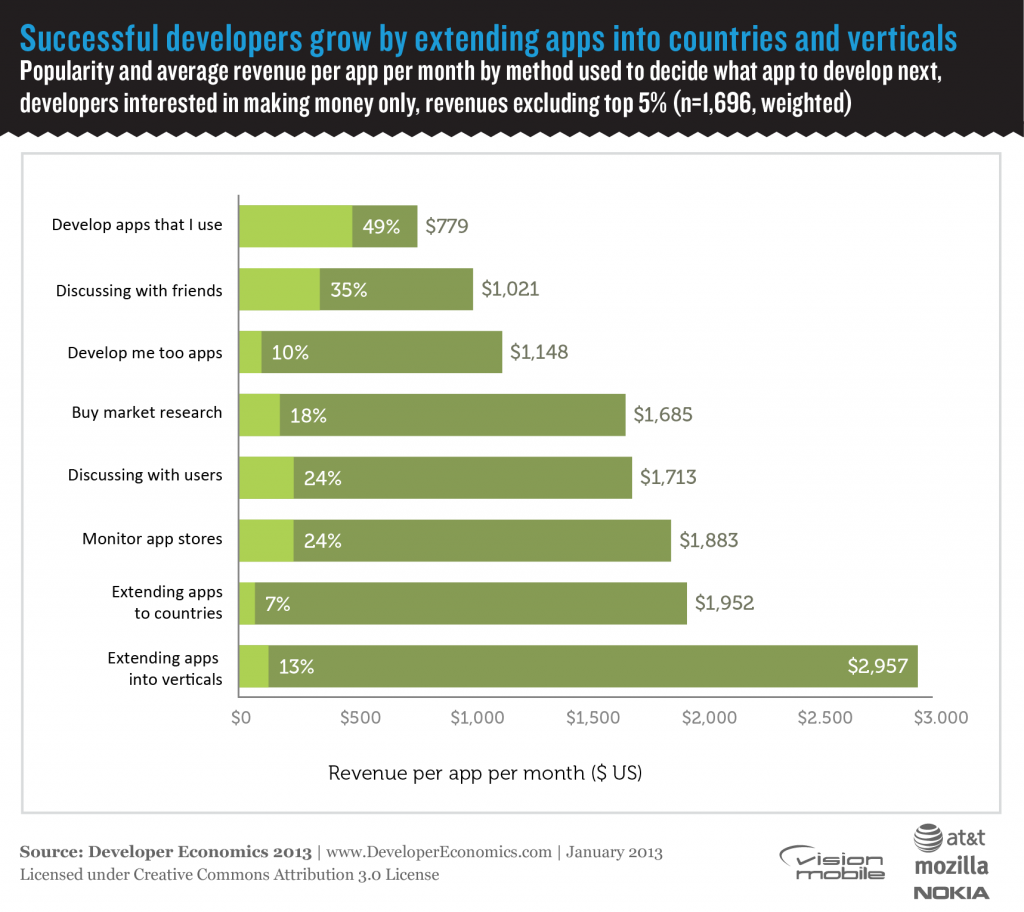

In our January 2013 Developer Economics Report, we revealed that multi-platform developers are better off. Our survey data also reveals, rather unsurprisingly, that users of cross-platform tools (CPTs) target more platforms than those building separate apps for each platform. Of those interested in making money, users of CPTs target 4.33 platforms (3.1 mobile platforms) on average vs 3.46 platforms (2.57 mobile) for those building separate apps. We also know that the most popular class of CPTs (using web authoring languages) tradeoff app capability to get the increased portability. At the same time, popular opinion on the internet and amongst venture capitalists is that a cross-platform user experience can’t compete with using the platform native frameworks. So how do these tradeoffs translate into revenue for CPT users?

CPT users make more revenue

On average, CPT users make slightly more revenue per app per month than developers not using such tools. With the reduced cost of development provided by the CPT, this suggests that they’re significantly more profitable.

Averages can be deceiving where the distribution of results is far from normal, as with app revenues, so it’s worth examining the details. App revenue is heavily concentrated at the top end of the market, with a large fraction of the (mean) average coming from a small number of very high earners. If we exclude all developers earning more than $50k per app per month then the result holds – CPT users still generate more revenue.

Not all CPTs are created equal

There are also several different types of CPT. Games have been responsible for close to half of all app revenues (at least those generated directly through app stores) and since they typically don’t require many platform-specific APIs or UI elements, they’re a good candidate for building with cross-platform. This suggests that users of primarily games-centric CPTs like Corona, Unity 3D & Marmalade might be responsible for the out-performance of CPTs, while users of the low development cost tools taking advantage of web authoring languages, such as PhoneGap, Appcelerator, Brightcove & Sencha, generate slightly lower revenues. However the data shows that the opposite is in fact the case. Users of the games-centric CPTs are generating below average revenue, whilst the web-centric CPT users are significantly better off. These results also hold whether or not we include those earning over $50k per app per month.

A plausible explanation for this is that most of the larger and more successful game developers are managing their own cross-platform compatibility or code re-use whilst many smaller independent game developers relying on 3rd party tooling are struggling with the fierce competition in the games market. At the same time it seems that, when it comes to revenue, a fully native user experience and native performance are not as important as their proponents suggest. The very high earners using web-centric tools are most likely to be existing publishers selling their content through mobile app subscriptions and our revenue estimates are probably too low, since the top income band in our survey is everything over $100k per app per month.

Both ends of the revenue spectrum

For several CPTs in our survey we didn’t have enough respondents to be sure differences in revenues for individual tools are statistically significant, however, there are a couple of individual ones worth highlighting. At the low end, revenues for Qt developers were significantly below average – this probably reflects the fact that Qt does not yet have official support for iOS or Android (planned for this year). At the high end, although we only had a relatively small sample, revenues for Brightcove App Cloud users were more than 3 times the average making the difference statistically significant, whether or not we include those generating over $50k per app per month. Brightcove appear to be focussing their solution on a particularly profitable market segment.

Tool selection – do it for the right reasons

Finally, if you’re looking to select a CPT, make sure you do it for the right reasons. Main selection criteria including access to native APIs and the ability to create a native UI look and feel are correlated with above average revenue, whilst the availability of third party extensions and choice of authoring languages are correlated with below average revenue. The former criteria look to minimise some weaknesses of the cross-platform approach whereas the latter criteria focus on reducing one-off costs. The latter are not necessarily bad reasons for choosing a tool but if they are amongst the most important reasons for your selection then it’s worth re-evaluating priorities. Work out what will enable the creation of the best product at acceptable cost rather than simply minimising cost. If the lowest possible development cost is critical to make the app concept viable then it’s probably time to come up with a higher value concept.